Introduction of Loan Against Property

Imagine you need a large sum—for business expansion, medical emergency, or education—but don’t want to sell your home or liquidate investments. A loan against property lets you use your property as collateral to unlock capital while retaining ownership. It’s a powerful tool—but also one that comes with responsibilities and risks.

In this post, we’ll explore everything you need to know about a loan against property: how it works, eligibility, pros & cons, the application process, legal nuances, and smart strategies to make it work in your favor. Let’s start.

What Is a Loan Against Property?

A loan against property (LAP) is a secured loan in which a lender advances funds to a borrower, taking the borrower’s residential, commercial, or industrial property as collateral. The borrower retains ownership, but the lender acquires a mortgage (or charge) over the property.

The loan amount is typically a percentage of the “market value” of the property. For instance, many banks in India allow up to 75% of property value under LAP. ICICI Bank

The tenure is often longer—up to 15 years in many cases.

Interest rates may be floating or fixed, depending on the lender’s terms.

Because the loan is secured, lenders are more confident in giving larger sums at relatively lower interest rates than unsecured borrowing.

Why Consider a Loan Against Property?

Using your property as collateral has several advantages—if used wisely:

Benefits

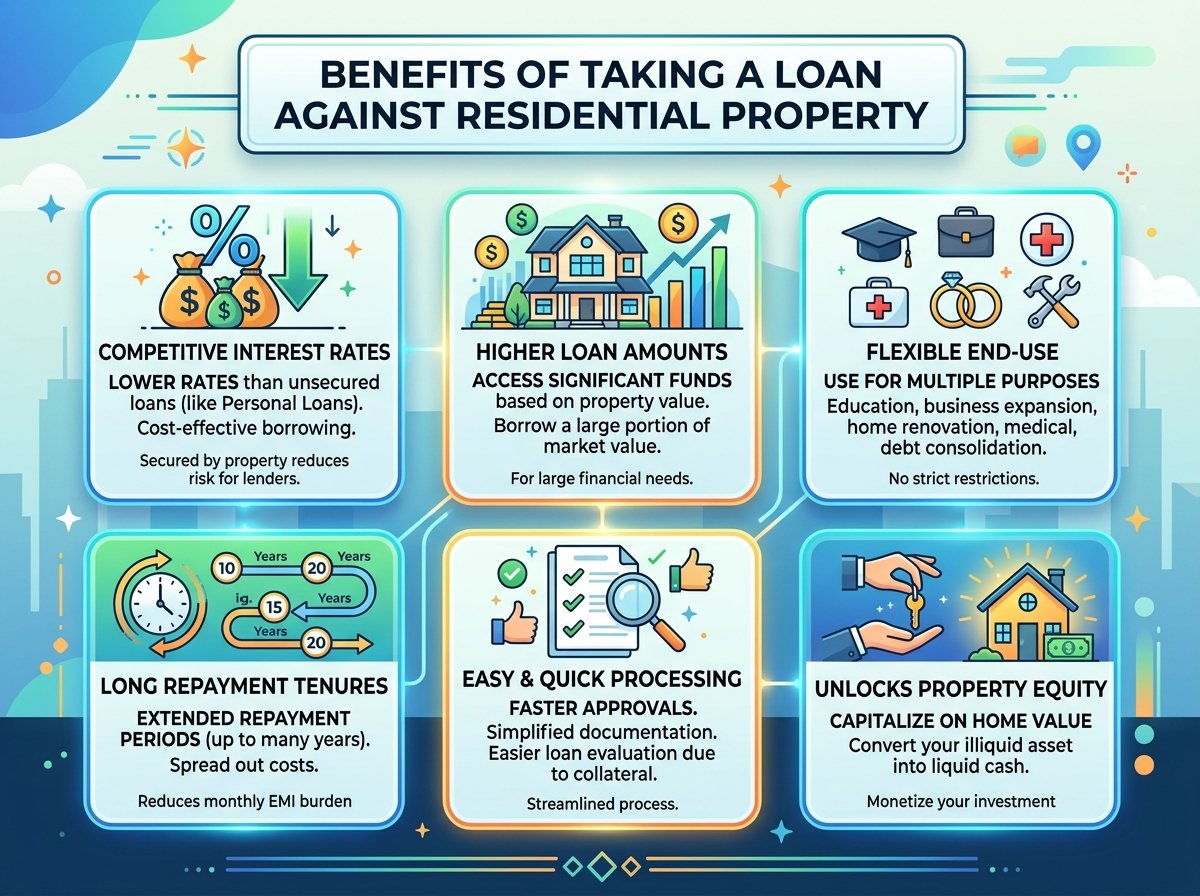

Higher loan amounts: Because it’s secured, banks may sanction large sums.

Longer tenure: Spreads repayment over years, reducing EMI burden.

Lower interest compared to unsecured loans: The security lowers the lending risk.

Flexible use of funds: Many lenders don’t restrict end use—business, health, education, etc.

You retain ownership and use: You can continue to live in or use the property while it’s mortgaged.

Risks & Considerations

Possibility of losing the property: If you default, the bank may foreclose or auction the collateral.

Valuation uncertainties: If property valuation is lower than expected, the loanable amount shrinks.

Processing, legal & stamp costs: These add to the effective cost.

Interest over a long period: Extended tenure means more interest paid overall.

Rigid eligibility criteria: Some borrowers may be turned down due to credit history, legal issues on property, or low income.

Eligibility Criteria & Key Parameters

To successfully secure a loan against property, lenders typically evaluate the following:

Key Requirements

Clear title & legal status of property

The property should be free from litigation or encumbrances.Good credit score / history

A higher credit score improves chances and may reduce the interest rate.Stable income / financial strength

For salaried or self‑employed individuals.Age & tenure constraints

Many lenders require borrowers to be between 21 and a maximum age (say 65 or 70) at loan maturity.Loan‑to‑Value (LTV) ratio

Most lenders finance only a portion of the property’s value (e.g., 60–75%).Property type & location

Residential, commercial, or industrial types; location, accessibility, and structural condition matter.Documentary support

Required documents include:Title deed, property tax receipts

Encumbrance certificate

KYC / identity / address proof

Income proof: salary slips, IT returns, audited statements

Bank statements, etc.

If any of these parameters don’t meet the lender’s norms, your application may get rejected or approved with less favorable terms.

How Much Can You Get & Loan Structure

Loan Quantum

Many lenders allow up to 75% of property value as a loan against property. ICICI Bank

Some NBFCs and banks may be more conservative, offering 60–70%.

The exact amount depends on your income, repayment capacity, credit history, and property valuation.

Repayment Tenure & EMI

Typical maximum tenure is 15 years in Indian banks. Longer tenure means smaller EMIs but higher total interest outgo.

Some lenders may permit overdraft / flexi facilities where you pay interest on the utilized portion only. ICICI Bank

Interest Rates & Charges

Rates differ by lender, property type, borrower profile, and whether the rate is fixed or floating.

For example, HDFC offers rates in the range of ~8.95%–10.25% depending on property and use. HDFC Bank

HSBC’s LAP offering includes floating rates for many cases.

Charges include processing fees (often 1% or so), legal and valuation fees, stamp duty, etc.

Some lenders allow no prepayment charges on floating rate LAPs.

Step-by-Step Process to Avail Loan Against Property

To make your LAP journey smooth, here’s a stepwise path:

Plan & research

Evaluate the approximate value of your property, your financial need, and EMI expectations.Shortlist lenders

Compare banks, NBFCs, interest rates, tenure options, and customer reviews.Check eligibility beforehand

Ensure your credit score, income, and property title are in order.Fill out the application & submit documents

Along with KYC, title deeds, income proofs, and property papers.Property valuation & legal check

Lender’s valuers & legal team verify the property’s market value and legal status.Loan sanction & offer letter

If all checks pass, the lender issues a sanction / approval letter with terms.Execution of mortgage documents

You execute the mortgage/mortgage deed (or charge creation) and register the documents.Disbursal of funds

Funds are transferred to you (or to the vendor if it is for property purchase) as per the agreement.Repayment & monitoring

Pay EMIs in time. If grace / moratorium is allowed, maintain clarity on when repayment begins.Closure / foreclosure

If you repay earlier, depending on the floating or fixed rate, prepayment/foreclosure rules apply.

Smart Tips & Best Practices

Get multiple valuation reports to avoid surprises

Negotiate processing fees and interest margins

Opt for floating rates if you believe interest rates may fall

Keep buffer in your income so EMI doesn’t strain your budget

Maintain backup documents and keep originals safe

Check for hidden charges: late fees, legal review costs, insurance

Try not to withdraw full tenure; borrow only what’s necessary

Understand prepayment/foreclosure conditions—if you pay early, what penalty may apply

Real‑Life Scenarios & Use Cases

Here are examples of how people use loans against property effectively:

A business owner mortgages his building to get working capital infusion without selling any asset

A family uses LAP to fund a child’s higher education abroad

Someone facing a medical emergency borrows via LAP rather than a personal loan at higher interest

Consolidation of high-interest debts (credit cards, personal loans) into a lower-cost LAP

Real estate investor improves or renovates property using LAP funds

These use cases make a loan against property a flexible tool—as long as risk is managed.

Risks, Mitigations & When to Avoid It

Major Risks

Default leads to foreclosure/seizure of property

Market downturn: property value decline reduces buffer

Overborrowing / overleveraging financial capacity

Legal / title issues emerging later

Hidden costs or charges

Mitigations

Borrow conservatively, not the maximum possible

Keep contingency funds to manage EMI disruptions

Ensure title and legal checks are thorough

Get insurance over the property

Read all terms, especially on prepayment/foreclosure.

When to Avoid LAP

If your income is volatile or uncertain

When title of the property is disputed or legally uncertain

If the interest rate is too steep relative to your earning capacity

If you foresee likely future obligations impacting cash flow

Conclusion & Call to Action

A loan against property can be a savvy financial tool—offering large funds at lower interest, longer tenures, and flexible usage—while you retain your property. But with the upside comes risk. Your success depends on careful planning, honest evaluation, and disciplined repayment.

If you’re thinking of applying for a loan against property, I can help:

Evaluate your eligibility

Pick the best bank/NBFC deal

Review your property & legal documents

Assist you in negotiating terms

Let me know if you’d like me to walk you through a personalized LAP strategy for your property!