Benefits of Taking a Loan Against Residential Property

What Is a Loan Against Residential Property?

A Loan Against Residential Property (LAP) is a secured loan where you pledge your residential property as collateral to obtain funds from a bank or financial institution. The ownership of the property remains with you while the lender provides a loan based on the property’s market value.

The loan amount generally ranges between 50% to 75% of the property’s value depending on the lender and your repayment capacity.

Why People Choose a Loan Against Residential Property

Unlike personal loans that often carry high interest rates and shorter repayment periods, a loan against residential property offers better financial flexibility.

People commonly use this loan for:

Business expansion

Medical emergencies

Children’s education

Wedding expenses

Debt consolidation

Home renovation

Working capital needs

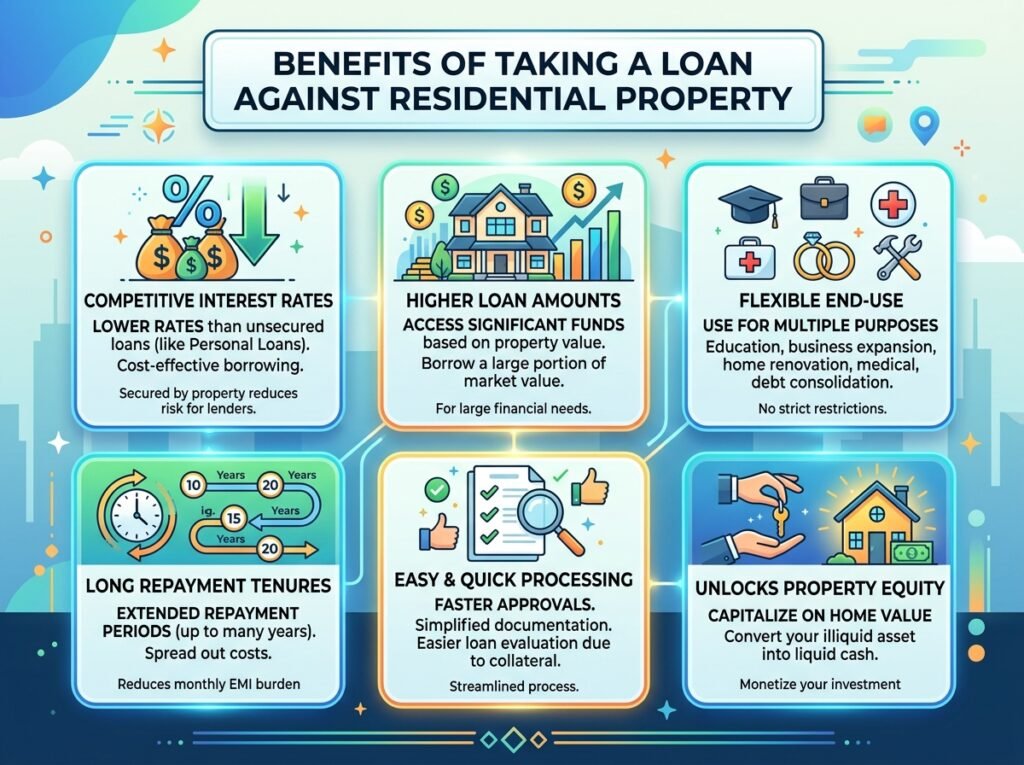

Major Benefits of Taking a Loan Against Residential Property

1. Lower Interest Rates Compared to Personal Loans

2. Higher Loan Amount Eligibility

3. Continue Owning and Using Your Property

4. Flexible Repayment Tenure

5. Multipurpose Loan Usage

6. Faster Loan Processing

7. Better Financial Management

8. Ideal for Self-Employed Individuals

9. Tax Benefits in Certain Cases

10. Improves Liquidity Without Selling Assets

Eligibility Criteria for Loan Against Residential Property

Although requirements differ among lenders, the common eligibility criteria include:

Basic Eligibility:

Indian citizen

Salaried or self-employed

Stable income source

Age usually between 21 and 65 years

Clear property title

Property Requirements:

Legally approved property

Marketable title

No major legal disputes

Documents Required

Here are the commonly required documents:

Personal Documents

PAN Card

Aadhaar Card

Passport size photographs

Income Documents

Salary slips

Income tax returns

Bank statements

Property Documents

Sale deed

Property tax receipts

Approved building plan

Ownership proof

Keeping documents organized can significantly speed up approval.

Important Things to Consider Before Applying

Before taking a loan against residential property, carefully evaluate these factors:

1. Interest Rate Comparison

Always compare multiple lenders before finalizing.

2. Loan-to-Value Ratio

Understand how much funding you can receive against your property’s value.

3. Processing Charges

Check for hidden fees and foreclosure charges.

4. Repayment Capacity

Borrow only what you can comfortably repay.

5. Property Valuation

Ensure your property documents are legally clear and updated.

Common Mistakes Borrowers Should Avoid

Borrowing more than needed

Ignoring hidden charges

Missing EMI payments

Not reading loan terms carefully

Choosing very short repayment tenure

Smart financial planning helps maximize the benefits of LAP.

Who Should Consider a Loan Against Residential Property?

This financing option is ideal for:

Small business owners

Families facing medical emergencies

Parents funding higher education

Professionals seeking working capital

Individuals consolidating debts

It is best suited for borrowers needing large funds at lower interest rates.

How Draft My Documents Can Help

At Draft My Documents, we help individuals simplify legal and financial documentation related to loans and property matters.

Our services include:

Property document assistance

Legal drafting support

Loan documentation guidance

Affidavits and agreements

Property-related legal paperwork

For professional assistance:

Draft My Documents +91 9016855337 +91 9867170895

Frequently Asked Questions

Is a loan against residential property safe?

Yes, it is considered safe if you repay EMIs on time and borrow responsibly. You continue owning the property throughout the loan tenure.

What is the maximum loan amount I can get?

Most lenders provide around 50% to 75% of the property’s market value.

Can I use the loan amount for business purposes?

Yes, funds can be used for business expansion, working capital, education, medical expenses, and other personal needs.

What happens if I fail to repay the loan?

Failure to repay may lead to legal recovery action, including possession of the mortgaged property by the lender.

How long does loan approval take?

If documents are complete, approval may happen within a few days depending on the lender.

Conclusion

The benefits of taking a loan against residential property make it one of the most practical financing solutions for individuals and businesses seeking substantial funds at lower interest rates. From flexible repayment terms and higher loan eligibility to continued property ownership and multipurpose usage, LAP offers significant financial advantages.

However, responsible borrowing and proper financial planning are essential to avoid repayment stress. Always compare lenders, understand terms carefully, and keep your property documents legally updated before applying.

If you need expert assistance with property documentation, legal drafting, or loan-related paperwork, connect with Draft My Documents today. You can find our website on Google.